Visa Stablecoin Integration 2026: How Companies Reduce Payment Costs by 99%

Key Takeaways

- 99% Cost Savings: International corporate transactions via stablecoin often cost under $0.50, while traditional banking channels (SWIFT) consume up to $65.

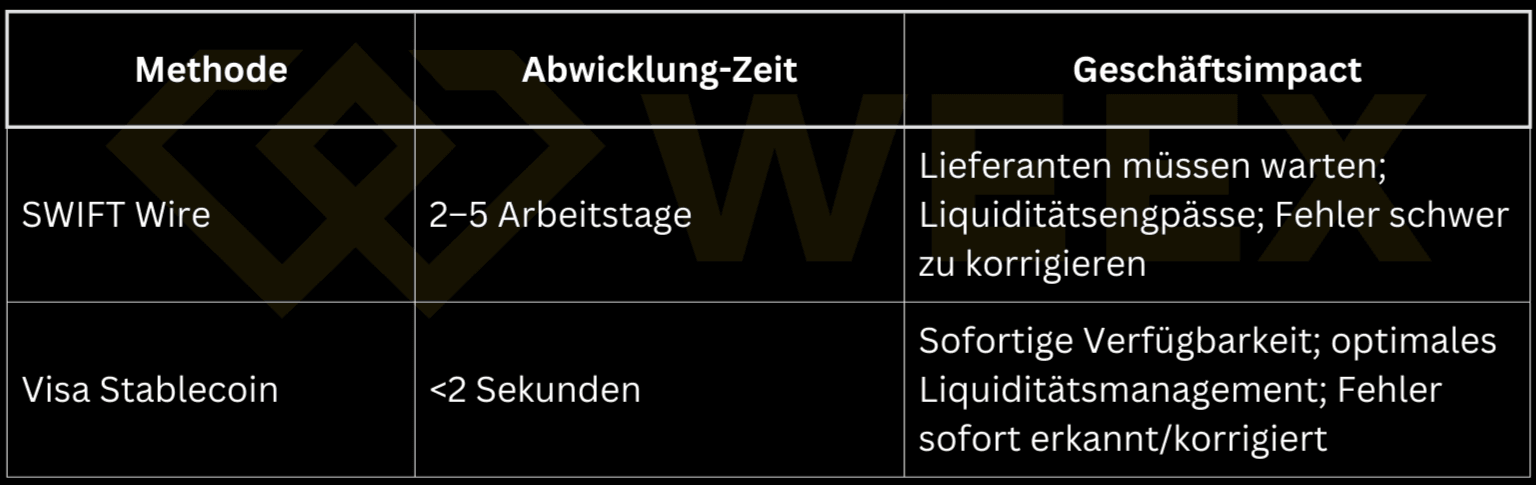

- Settlement in Seconds: Instead of waiting 2–5 days for bank confirmations, payments via Visa-integrated blockchains (e.g., Solana) occur in under 2 seconds.

- Legal Certainty 2026: With the full applicability of MiCA (EU) and the GENIUS Act (USA), companies now use stablecoins within a legally secure, regulated framework.

- Strategic Flexibility: Visa’s four-pillar model (VTAP) supports diverse blockchains (Ethereum, Solana) and currencies (USDC, EURC, PYUSD) for every business case.

- Simple Integration: Via APIs, blockchain infrastructure can be integrated directly into existing ERP and accounting systems without companies needing to be crypto experts.

Introduction

Since 2024, Visa has enabled companies to process international payments directly via stablecoins like USDC – without SWIFT delays and without high bank fees. The numbers are clear: transactions cost under $0.50 instead of $6.49, take 2 seconds instead of 5 days, and save companies with 1,000+ payments annually over $60,000.

But how does Visa Stablecoin Integration actually work? Which blockchains are supported? And how do companies meet MiCA and GENIUS Act requirements in 2026?

This guide explains Visa’s four-pillar strategy, shows the step-by-step implementation, and compares USDC, EURC, and PYUSD based on real-world use cases.

What is Visa Stablecoin Integration?

Visa Stablecoin Integration is the combination of Visa’s global payment infrastructure and digital, value-stable currencies (stablecoins) like USDC. It allows companies to send payments directly via the blockchain – faster, more transparently, and more cost-effectively than through traditional correspondent banks.

Unlike classic credit card transactions, there is no lengthy intermediary process here. The money moves directly from wallet to wallet, while Visa provides the compliance, security, and settlement logic.

The Four Pillars of the Visa Stablecoin Strategy

Visa’s strategy for 2025/2026 is based on four central pillars that connect traditional finance (TradFi) with the blockchain world (DeFi).

1. Settlement

Visa enables financial institutions to exchange stablecoins directly with one another. An example: Bank A in Zurich sends USDC on WEEX directly to Bank B in Singapore. Instead of using the SWIFT network (2–5 days), the settlement occurs directly on the blockchain.

2. Issuance

Via the VTAP (Visa Tokenized Asset Platform), banks can issue their own stablecoins – e.g., a “Digital Euro” or an institutional token for internal clearing. This is particularly relevant for central banks that want to control their own digital currencies (CBDCs).

3. Cross-Border Payments

This is the core business: cross-border payments without bank intermediaries. Visa cooperates here with partners such as Aquanow for the CEMEA region (Central Eastern Middle East Africa) to make remittances more efficient.

4. Platform (VTAP for Banks)

The Visa Tokenized Asset Platform is the technical foundation – an open ecosystem for banks to manage stablecoins. Major banks like BBVA are already using VTAP to modernize their infrastructure.

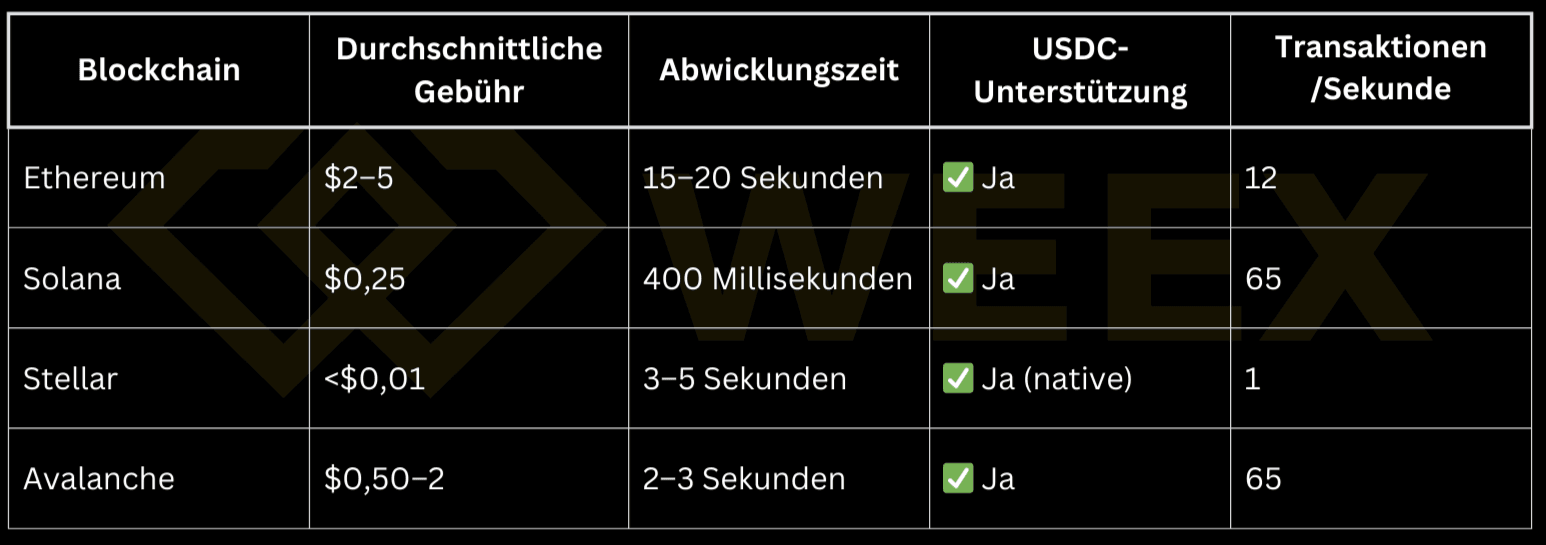

Supported Blockchains & Stablecoins Compared

Visa relies on a multi-chain strategy to avoid dependence on a single blockchain. Depending on the use case, different networks are suitable.

Blockchain Comparison: Which is the best?

Users should evaluate which blockchain is best for stablecoin payments before starting a technical integration.

Which stablecoin fits my company?

The choice of coin depends heavily on the geographic focus.

- USDC (Circle): The gold standard for B2B. 1:1 backed by US dollars and highly regulated. Learn more about what Circle is and how USDC works.

- EURC (Circle): Ideal for European companies that want to avoid exchange rate risks against the Euro.

- PYUSD (PayPal): Relevant for e-commerce merchants already integrated into the PayPal ecosystem.

- USDG: A fee-efficient alternative for specific markets.

Implementation: How companies integrate Visa stablecoin payments

The transition to blockchain settlement occurs in five structured phases.

- Compliance & KYC (2–4 weeks): Every company must undergo full verification. This protects against money laundering and secures bank partnerships. This is how KYC works at WEEX and other financial service providers: identity verification and audit of the source of funds are standard.

- Wallet Infrastructure: You need either a self-custody wallet or a custodian like Fireblocks. For beginners, secure wallet solutions for companies are available that minimize technical hurdles.

- API Integration (2–8 weeks): Connect your ERP system (e.g., SAP, Oracle) to the blockchain via Visa’s APIs. This enables automatic payment reconciliation.

- Pilot Phase: Start with small transactions ($1,000–$10,000) to test process reliability.

- Live Operation: After a successful test, the rollout to the entire payment volume follows.

Practical Examples: 3 Use Cases with ROI Calculation

How much does the integration really save? Here are three scenarios based on market data from 2025.

Use Case 1: International Supply Chain

A German manufacturing company pays 100 Asian suppliers monthly.

- Before (SWIFT): $50 fee per tx × 100 = $5,000/month. Waiting time: 3–5 days.

- After (USDC via Solana): $0.25 per tx × 100 = $25/month. Waiting time: 2 seconds.

- Savings: $59,700 per year + improved supplier relationships through instant payment.

Use Case 2: Freelancer Payroll

A tech startup pays 50 developers worldwide.

- Before (Wise/PayPal): 3–5% fees on $100,000 volume = ~$4,000/month.

- After (Stablecoin): <0.5% fees = ~$500/month.

- Savings: $42,000 per year.

Use Case 3: Treasury Management

A corporation distributes $100 million in liquidity to subsidiaries. Instead of manual bank transfers, they use smart contracts for automatic allocation. The result: real-time liquidity overview and minimization of FX risks.

Regulation 2026: GENIUS Act & MiCA in Detail

Regulatory uncertainty is over. In 2026, clear rules for stablecoins apply in the most important markets.

USA: GENIUS Act (July 2025)

The “GENIUS Act,” signed on July 18, 2025, creates a federal framework for the first time. It requires 1:1 reserve backing for payment stablecoins and registration with the Federal Reserve. For companies, this means maximum legal certainty for USD transactions. Read more about GENIUS Act: The new US stablecoin regulation.

Europe: MiCA (Markets in Crypto-Assets)

Fully applicable since the end of 2024, MiCA regulates stablecoins as E-Money Tokens (EMTs). Issuers must hold strict liquidity reserves. Companies should check which MiCA requirements for stablecoins their partners must meet to remain compliant in the EU.

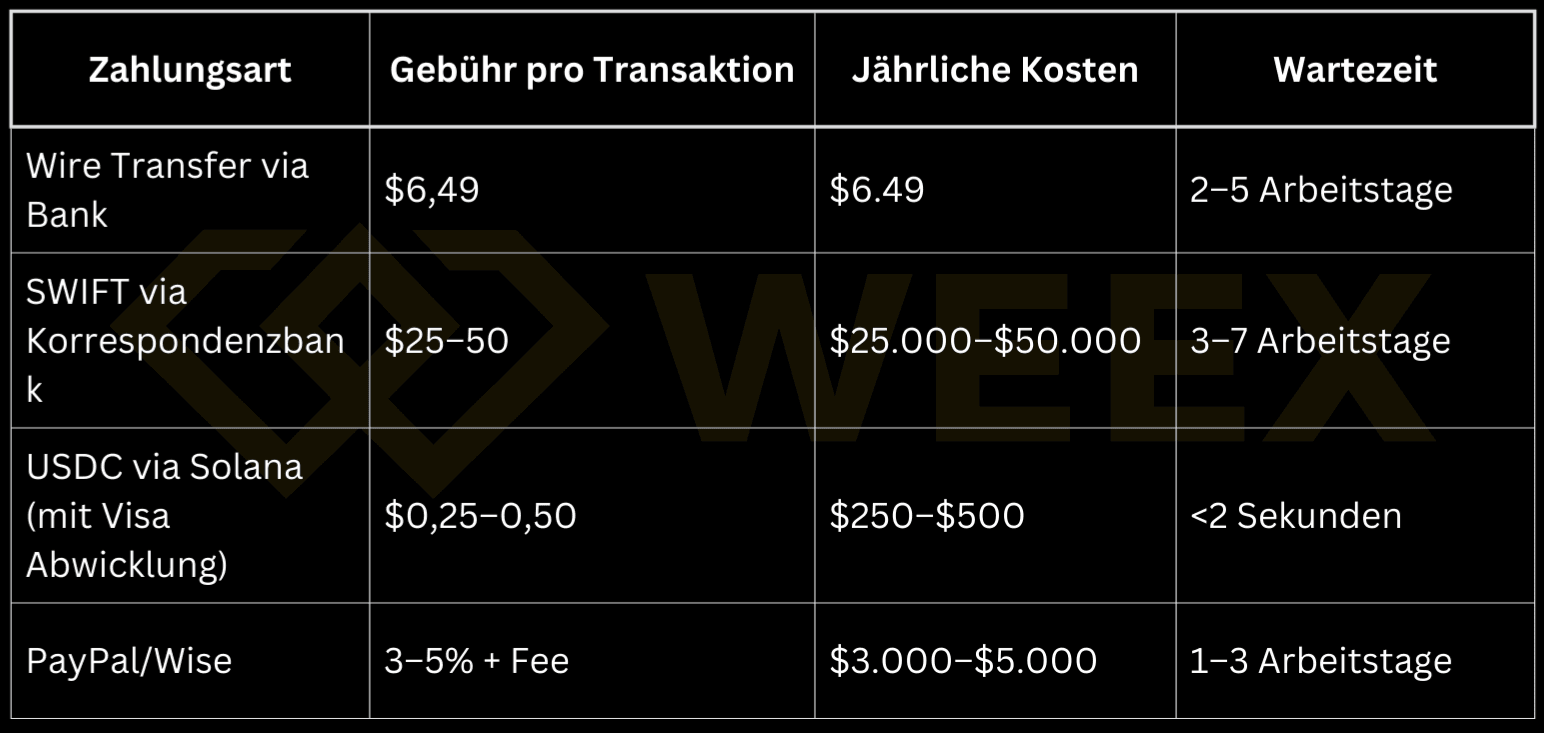

Cost Comparison: Stablecoin vs. SWIFT vs. PayPal

For a company with $100 million annual volume (approx. 1,000 transactions of $100,000 each):

Pro-Tip: What do you do with stablecoins that are not currently being sent? Use services like USDT passive interest with WEEX Auto Earn to receive daily yields on unused capital.

WEEX: Trade, stake, and use stablecoins for payments

WEEX bridges the gap between professional trading and using stablecoins for payments. While Visa provides the infrastructure for payments, WEEX provides the liquidity and tools to manage your assets.

- Liquidity Management: Buy and sell large amounts of USDC or EURC with minimal slippage via our spot market.

- WXT Token: Use WXT: The WEEX token with trading benefits to further reduce fees when converting fiat to stablecoins.

- Copy-Trading: While your treasury waits for the next payment run, you can use parts of the capital and copy elite traders and benefit from stablecoin strategies.

Test WEEX as your primary interface for crypto liquidity in the DACH region.

Frequently Asked Questions (FAQ)

What is the difference between USDC and USDT?

USDC (Circle) is considered more regulated and transparent (1:1 USD backing, monthly audits), which makes it ideal for Visa partnerships. USDT is more liquid but often less transparent in its reserve structure.

Can I start with Visa stablecoin settlement immediately?

Not immediately. Your company must first choose a suitable wallet partner and undergo the KYC/AML process. Expect 2–4 weeks of onboarding time.

How secure are stablecoin transactions via Visa?

Very secure. You use the established security infrastructure of Visa combined with the immutability of the blockchain. All transactions are permanently logged and auditable.

Is stablecoin settlement legal in Germany?

Yes, through the MiCA regulation, the use of regulated stablecoins (E-Money Tokens) is legally secure in the EU and Germany.

WEEX | Rising Star of Crypto Exchanges in the DACH Region

WEEX combines security, innovation, and community with features for beginners and professionals:

Security & Protection

- 1,000 BTC Protection Fund: Self-funded reserve for rapid loss protection in exceptional cases

Trading & Earning

- Auto Earn: Daily automatic USDT earnings without effort

- Copy-Trading: Follow elite traders automatically or apply as an elite trader for additional benefits

- WE-Launch: Early access to new projects – exclusive for WEEX users

Benefits & Rewards

- Promotions & Rewards: Trading competitions and special bonuses for active users

- Affiliate Program: Lifetime commissions from new users – details here

- VIP Benefits: Lowest fees, market insights, and personal support for high-volume traders

- WXT Token: Fee discounts, airdrops, and exclusive platform benefits

Discover current trends on WEEX Spot and start now: Register now

Disclaimer – Legal Notice from WEEX Exchange

WEEX and its affiliates offer services for the exchange of digital assets, including derivatives and margin trading, only where legal and to eligible users. All content is general information, not financial advice – seek independent advice before trading. Trading cryptocurrencies involves high risk and can lead to a total loss. By using WEEX services, you accept all associated risks and conditions. Never invest more than you can afford to lose. Further information can be found in our Terms of Use and in the Risk Disclosure.